- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Why do medical practices sell to equity funds?

As hospitals and investors look to buy physician offices, there are strategies for doctors to maximize the purchase price.

© Valeri Luzina - stock.adobe.com

Physician practices across the country are being courted by a number of potential buyers who have strategic interests in owning a medically related enterprise. Physicians are turning to equity funds as buyers because equity funds typically pay more for a practice than any other form of buyer. Physicians need to understand why equity funds can pay more for a practice than can be paid by a hospital, and the steps necessary to maximize the purchase price paid by the equity fund.

Hospitals as buyers

Hospitals and equity funds are continually looking to acquire medical practices. From a practical perspective, hospitals typically cannot pay as much for a medical practice as the practice can receive from an equity fund. This is because the federal government carefully monitors whether payments by a hospital to a physician or physician group are excessive and will constitute a direct or indirect inducement for patient referrals in violation of the federal Anti-Kickback Statute.

Randal Schultz, Esq.

Hospitals are allowed to pay a "fair market value and commercially reasonable" purchase price for a practice or as compensation to a physician without violating the Anti-Kickback Statute. A fair market value and commercially reasonable purchase price essentially equates to what a willing buyer would pay to a willing seller for the hard assets of the practice. This definition creates a great amount of controversy in many hospital/physician transactions and is dramatically lower than the price typically offered by the equity fund.

No referrals necessary

Conversely, given a physician cannot make patient referrals to an equity fund and the equity fund cannot make referrals to the physician, the Anti-Kickback Statute is usually not implicated in an equity fund/physician practice deal. Therefore, physician practices are often sold at a six- to 12-times multiple of the practice’s earnings before interest, taxes, depreciation and amortization. Known as EBITDA, that essentially is cash available after payment of all expenses including an agreed amount for physician compensation. The ultimate goal of the equity fund is to purchase multiple medical practices and, thereafter, combine whatever EBITDA can be removed from the medical practices and sell the aggregated EBITDA to yet a larger equity fund for a 10- to 16-times multiple. The spread between what the equity fund pays for the medical practices and the price it can receive when selling the aggregated practices to the larger fund, is what is driving this surge in acquisitions of medical practices by equity funds.

Primary care practices and assets

When representing primary care medical practices, we work with the medical practices to enhance their attractiveness to both hospitals and equity funds. To attract hospitals, the primary care practice needs to be responsible for directing the medical services for as many covered lives as possible or provide some type of service that is unique in the marketplace. The U.S. Supreme Court clearly states that if even one purpose of the payment by a hospital to a medical group is to induce patient referrals, the payment is illegal. Therefore, it must be made clear that the acquisition of the primary care practice is to assure appropriate coverage for people in the hospital's service area needing primary care services and not for the purchase of referrals and that the payment constitutes fair market value consideration for what is being purchased.

Additionally, hospitals may want to acquire office buildings, land, equipment or other assets under the control of the primary care group. Each of those items can be acquired at a price equal to what an independent third party considers fair market value. Thus, the more tangible assets owned by a medical practice or by the physicians who own the medical practice, the greater the aggregate sum the hospital can pay to the physicians. The strategy is to allocate as much of the purchase price to the fair market value of these hard assets as possible to mitigate a claim that the hospital is paying for referrals by paying more for the medical practice itself than would be considered fair market value.

Physician salaries

Hospitals also try to attract physicians and their practices by offering higher salaries than the physicians historically earned in private practice. The concept is to compete with the equity funds purchasing power by paying higher salaries than are offered by the funds. However, the salaries a hospital can pay the physicians are also limited by the Anti-Kickback Statute. Consequently, the hospitals seek compensation guidelines from valuation companies and national physician compensation surveys to justify the offered salaries. Despite arguments by some commentators that the compensation surveys report artificially high salary ranges (the idea is that salaries reported by physicians to surveyors are overstated because the physicians believe the higher survey numbers will result in the hospitals’ ability to pay higher wages), hospitals have been successful in paying higher salaries than what physicians are usually paid in private practices (excluding physician’s income from ancillary services).

Physician practices that desire to stay private and avoid hospital control, hospitals in rural communities who are losing physicians to bigger cities, and equity funds often claim that larger urban hospitals use revenue from facility fees to inappropriately subsidize the higher physician salaries. The theory is that in return for higher salaries, the physicians are induced to maximize referrals to their employer hospital, which some commentators suggest is a disguised violation of the Anti-Kickback Statute. Hospitals cannot use facility fees to pay excessive physician salaries.

Hospitals have been able to acquire primary care physicians at a faster rate than acquiring specialists’ practices because, typically, primary care physicians do not have the same access to ancillary income opportunities available to specialists. Thus, the salaries of private practice primary care physicians are typically lower than the income of many specialists, enabling the hospital to employ primary care physicians at lower cost to the hospital and at an increased rate of pay for the physicians.

Maximize EBITDA for private equity investment

Although hospitals may claim that the acquisition of physicians and physician practices is intended to enhance patient care in the community (they deny a focus on obtaining additional facility fees), the equity fund is typically openly motivated by creating a financial return for itself and the physicians. A business strategy for every physician group seeking a sale to an equity fund is to find a way to maximize its available EBITDA because the available EBITDA is often sold to the equity fund at a six- to 10-times multiple. Thus, the higher the EBITDA, the higher the purchase price.

Maximizing EBITDA requires the use of qualified advisers who have experience with these types of transactions. Maximizing EBITDA focuses on the practice's income statement to determine how to reduce expenses and increase revenue so that the profit available to the equity fund is maximized. Does the practice have excess staff or use outside services that are in excess of what is needed to appropriately run the practice? Mathematically, decreasing office expenses directly increases EBITDA. If the physicians own the medical office building to which the practice is paying rent, a reduction in office rent will increase the EBITDA. For every dollar increase in EBITDA, there is a corresponding increase in the purchase price by multiplying the increase in EBITDA by the multiple offered by the equity fund. The strategy is to find every expense incurred by the practice that can be reduced or eliminated, without affecting the delivery of patient services, that can result in an increase to practice EBITDA.

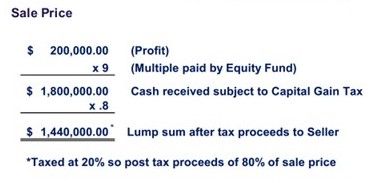

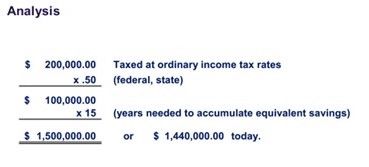

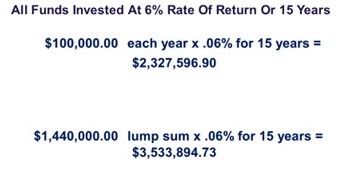

Dollars and cents: an example

Equations provided by Randal Schultz, Esq.

The foregoing example illustrates the financial power of a proposed equity fund transaction. In addition, the equity fund will often pay the $1.8 million described above partly in cash and partly in stock of an entity affiliated with the equity fund. The strategy is to accumulate multiple practices to sell to a larger equity fund. By offering part of the purchase price in stock in contemplation of a future sale, the physicians stay employed by the fund in anticipation of a second enhanced payday. Thus, the equity fund argues that the physician is not only earning the nine-times multiple on the initial sale, but to the extent the physicians also receive stock and it sells in the future at a much higher multiple, the physicians receive an even greater return.

Once the maximum EBITDA is determined and the resulting maximum purchase price is achieved, the task is to assure as much of the purchase price as possible is taxed at long-term capital gains rates. Long-term capital gains rates are achieved through sales of stock of a practice (however, equity deals are usually “asset sales” due to corporate practice of medicine restrictions and buyer adversity to acquiring unknown liabilities) or asset sales that appropriately maximize the allocation of the purchase price to payments for “goodwill.” It is also critical to assure that any purchase price paid, in part, in the form of equity fund stock is received by the physicians in a tax-free exchange. A knowledgeable tax adviser is critical for this purpose.

Strategies for small groups

Understanding the foregoing is the basis for planning the future business sale of a medical practice. Assuming physicians do not have office or rent expenses they can reduce or eliminate to create EBITDA, and assuming they do not have large salaries they can reduce to create EBITDA, the strategy is to find EBITDA in other ways. A common strategy is for small groups to combine to become larger groups to create economies of scale and, thereby, reduce expenses and create EBITDA. Some practices form management companies to manage other practices and use the resulting income as EBITDA. Leveraging mid-levels and engaging in telemedicine has also become a source of revenue that can create EBITDA. Exploring these strategies will be addressed in a future article.

Conclusion

Given the change in the way financial markets reward innovation, which has caused equity players to enter into new types of businesses, health care has become an industry of choice due to the continued patient need for services and the resulting stable stream of income. Physicians and health care entities of all types need to carefully review this emerging market trend and plan for these new opportunities.

Randal Schultz, Esq., partner at Lathrop GPM, is a seasoned transactional and regulatory health care industry lawyer with 30 years of experience. He has counseled health care organizations of all types across the country for the development of business/financial structures, entity formation, program/product creation, equity transactions and regulatory compliance.